Obesity Is a Catalyst for Change: Imaging the New Era of GLP‑1 Trials

Obesity Is a Catalyst for Change: Imaging the New Era of GLP‑1 Trials

How a disease the world once dismissed as a lifestyle choice became the most consequential force reshaping medicine, markets, and what it means to grow old.

The story of obesity in 2026 is not a story about weight. It is a story about power – the power of a reclassified disease to force an entire industry to rebuild itself from scratch. It is about two pharmaceutical companies that transformed into trillion-dollar platforms in five years. It is about a drug class that began as a diabetes tool, became a weight-loss phenomenon, and is now being seriously discussed as the first medication that could slow the biology of human aging. And it is about a commercial model so unusual, drugs paid for largely out of pocket, by choice, at scale, that it has no real precedent in pharmaceutical history.

Every element of this story has implications for how drug developers design trials, how imaging endpoints get selected, and how clinical evidence gets built. The companies that understand this landscape and move early will define the next decade of metabolic medicine.

The Paradigm Collapse: From Moral Failing to Chronic Disease

For as long as medicine had a waiting room, obesity sat in it quietly – misclassified, undertreated, and buried under decades of cultural stigma. The standard tool was a number: the Body Mass Index. If your BMI exceeded 30, you were obese. If it cleared 25, you were overweight. Simple arithmetic made a complex biology look manageable, and the prescription was straightforward: eat less, move more.

That framework has finally been dismantled. In January 2025, a commission of 58 scientists from around the world published a landmark framework in The Lancet Diabetes & Endocrinology that called for a fundamental rethinking of how obesity is defined and categorized. BMI, the commission argued, should be a screening tool at best, not a diagnosis. In its place, clinical evaluation should incorporate waist circumference, waist-to-hip ratios, and where necessary, body composition imaging such as DEXA scans. More importantly, patients should be stratified into two distinct groups: those with pre-clinical obesity, where excess adiposity has not yet damaged organs, and those with clinical obesity, where the fat burden is actively harming cardiovascular, metabolic, musculoskeletal, or neurological function (CNN, 2025).

The distinction sounds academic. It is not. When you separate pre-clinical from clinical obesity, you create a treatment hierarchy with clear pharmacological triggers. You expand the population eligible for intervention. You remove the physician’s hesitation to prescribe. And you dismantle the stigma that has long caused patients to avoid seeking help altogether. Research published in Diabetes, Obesity & Metabolism tracked Danish patients from 2022 to 2024 and found that as treatment options improved, patients became far more willing to raise weight-related concerns with their doctors, a behavioral shift that has no historical parallel in this disease area (Diabetes, Obesity & Metabolism, 2026).

When a disease goes from moral failing to medical diagnosis, everything downstream changes: insurance coverage obligations, prescribing patterns, regulatory approval pathways, and critically, the design of clinical trials.

Body composition, organ fat distribution, hepatic steatosis, and metabolic biomarkers all become legitimate endpoints. Imaging becomes central. This is where the story stops being philosophical and starts being commercially urgent.

The Science of the Moment: What GLP-1 Actually Does

The glucagon-like peptide-1 receptor agonist was approved for type 2 diabetes a quarter of a century ago. Nobody in 2001 imagined it would one day be the world’s best-selling drug and a genuine candidate for the title of the first longevity medicine. That journey tells you something about how dramatically biology can outpace its original commercial brief.

The mechanism is, at its core, a masterclass in mimicry. GLP-1 agonists replicate a gut hormone that the body produces naturally after eating. They stimulate insulin release, suppress glucagon, slow gastric emptying, and the critical piece for obesity in signaling satiety to the brain. The result is profound: patients eat less not because they are trying to, but because the neurological hunger signal has been pharmacologically quieted. When Eli Lilly’s tirzepatide, a dual agonist that targets both GLP-1 and glucose-dependent insulinotropic polypeptide (GIP) receptors was evaluated in the SURMOUNT-1 trial, participants lost an average of 22.5% of body weight at the highest dose. That number had never appeared in a pill trial before. Bariatric surgeons were the only ones who had seen figures like it (Reviews in Cardiovascular Medicine, 2025).

The pipeline racing to build on that foundation is formidable. Survodutide from Zealand and Boehringer Ingelheim – a dual GLP-1/glucagon receptor agonist is in Phase 3 for both obesity and liver disease, with an FDA decision possible as early as 2027. Amgen’s Maritide and Viking Therapeutics’ VK2735 are in Phase 3 for obesity, with oral and injectable formulations in development. Novo Nordisk launched the world’s first oral GLP-1 for weight loss in early 2026. Eli Lilly’s orforglipron, an oral small molecule, not a peptide – is expected to receive FDA approval this year and has already prompted Lilly to build three new dedicated manufacturing facilities in the United States (Prime Therapeutics, 2025).

The industry is moving through innovation waves at unusual speed. First came injectable biologics. Now come oral pills. Next will come multi-receptor agents targeting GLP-1 alongside glucagon, amylin, and leptin receptors simultaneously – with the goal of 30%-plus body weight reduction. Further out, tissue-selective agonists are being designed to act primarily in the brain, separating efficacy from the gastrointestinal side effects that remain the main reason patients stop treatment.

Each wave brings a larger, more adherent, more treatment-seeking population. Each wave generates more clinical trial activity, more imaging endpoints, more need for centralized, validated, and reproducible evidence.

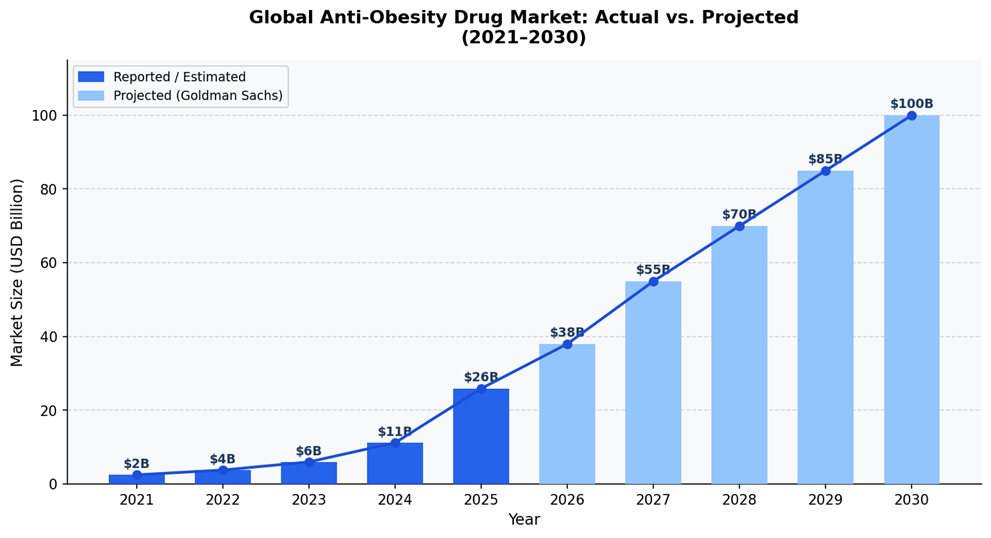

The US market alone was worth $11.2 billion in 2024 and is projected to reach $48.5 billion by 2030 – a CAGR of 24.2% (GrandView Research, 2025). Goldman Sachs had projected a $100 billion global market by 2030, though more recent forecasts have revised that figure to around $105 billion as price competition intensifies (Reuters, 2026). Even the downward revisions describe one of the fastest-growing pharmaceutical markets ever recorded.

The Out-of-Pocket Economy: A Market Unlike Any Other

Here is the fact that changes everything about how you analyze this market. The vast majority of GLP-1 obesity drugs are not covered by insurance. Patients buy them themselves.

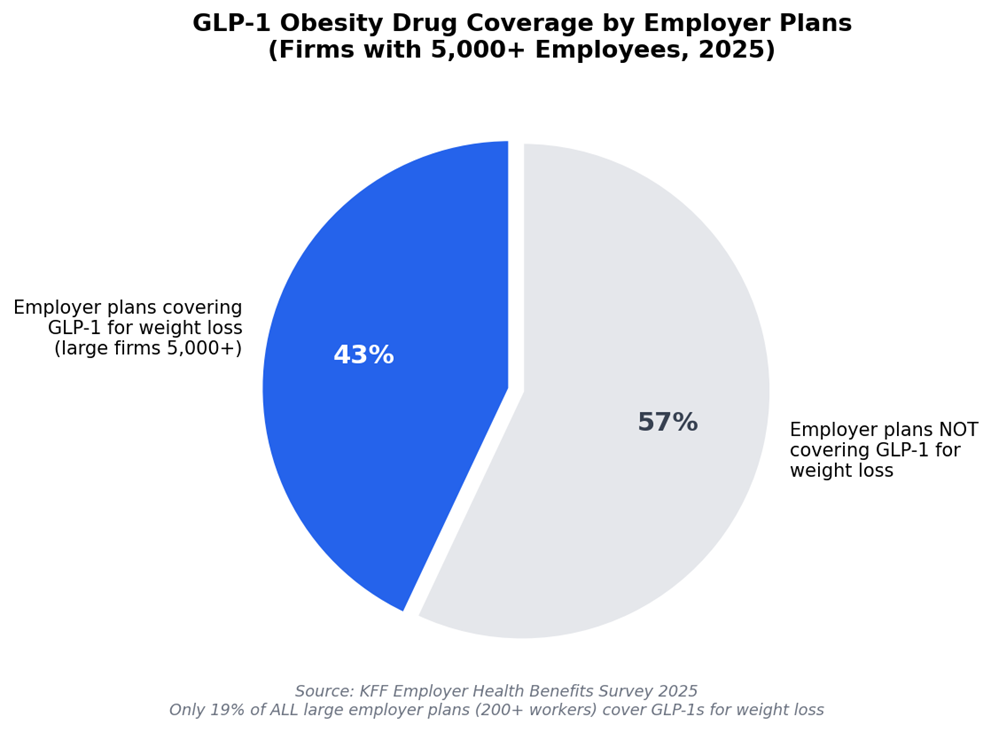

That is not a temporary anomaly waiting to be resolved by a policy change. It is a structural feature of the US healthcare system that has been in place for years and will remain in place – at least partially for years more. The Affordable Care Act does not require insurers to cover obesity medications. Medicare, the government insurer for the elderly, is legally barred from covering weight-loss drugs, though it does cover GLP-1s prescribed for diabetes, cardiovascular disease, and sleep apnea. Only 19% of large employer health plans covering 200 or more workers include GLP-1s for weight loss as of 2025 and even among the biggest employers, with 5,000 or more staff, only 43% provide this coverage, up from 28% the prior year (Peterson-KFF Health System Tracker, 2025).

In 2024, 62% of insurance requests for GLP-1 obesity medications were rejected (Oana Health, 2024). Among those with health insurance who took these drugs anyway, 27% paid the full cost out of pocket (KFF, 2025). A study in JAMA Health Forum found 40% of GLP-1 prescriptions went unfilled because patients simply could not afford them – even among insured patients, where average out-of-pocket costs still ran nearly $72 per prescription (Medical Xpress, 2025).

The list price for Zepbound is approximately $1,086 a month. Wegovy is approximately $1,000. Those prices did not kill demand.

They restructured it.

Between 2022 and early 2025, as the FDA permitted compounding pharmacies to produce these drugs under shortage conditions, a shadow market emerged offering semaglutide and tirzepatide through telehealth platforms for as little as $99–$299 a month.

IQVIA data found that patients seeking obesity treatment represented 83% of the entire compounded GLP-1 market during this period (IQVIA, 2025). Tens of billions of dollars in consumer spending moved through channels that did not show up in standard pharma market data.

In November 2025, the Trump administration brokered a direct deal with Lilly and Novo Nordisk, establishing a $149 per month price point for Medicare, Medicaid, and self-pay patients. Lilly’s own direct-to-consumer platform, LillyDirect, now sells Zepbound vials starting at $299 a month – available at 4,700 Walmart pharmacy locations as well as online and by Q2 2025 was already fulfilling approximately 35% of all new Zepbound prescriptions through this channel (CNBC, 2025; Walmart, 2025).

The strategic implication here is one of the most important in modern pharma.

A company that wins the out-of-pocket obesity market has not just found customers – it has built a direct consumer relationship, unmediated by payers, that confers pricing power and brand loyalty unavailable in any other therapeutic category.

It is priced not like a hospital drug but like a premium fitness subscription. And because obesity is chronic, requiring indefinite treatment to maintain results, the lifetime value of each patient is extraordinary.

Lilly and Novo Nordisk: The Anatomy of Exponential Growth

It is worth pausing on the numbers, because they do not feel real until you lay them side by side.

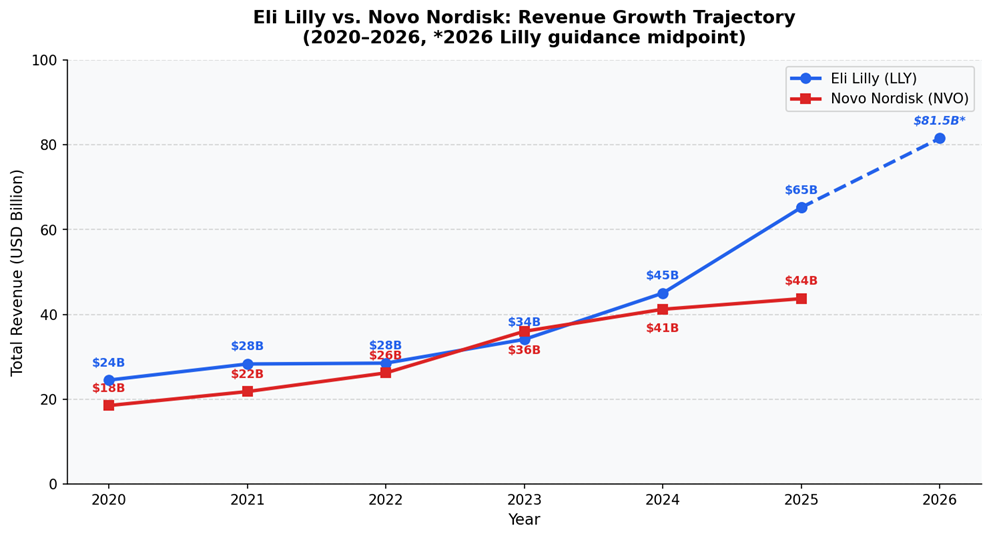

Eli Lilly’s total revenue in 2020 was $24.5 billion. Five years later, in 2025, it reached $65.2 billion – a 166% increase, with a 45% surge in the final year alone (Pharmaceutical Technology, 2026). Tirzepatide, sold as Mounjaro for diabetes and Zepbound for obesity, generated $36.5 billion in combined sales in 2025 making it the single best-selling drug in the world, ahead of Merck’s Keytruda at $31.7 billion (BioPharma Dive, 2026). For 2026, Lilly has guided revenue of $80–83 billion. The company’s market capitalization crossed $1 trillion in 2025. It is committing $27 billion to new US manufacturing infrastructure, with at least three facilities dedicated to incretin medicines.

Novo Nordisk’s trajectory has been remarkable on its own terms, though recent months have introduced more turbulence. Obesity care sales rose 26% in 2025 to DKK 82.3 billion, and the company still holds a branded volume market share of 59.6% across the global GLP-1 obesity market (Novo Nordisk Annual Report 2025). But CagriSema, its next-generation combination therapy failed to beat tirzepatide in head-to-head comparisons, and its 2026 guidance projects an adjusted sales decline of 5–13%, sending the stock down 61.8% over 12 months to early 2026. Novo launched the world’s first oral GLP-1 for weight loss in early 2026 and has entered a $2.1 billion partnership with Vivtex to develop next-generation oral biologics, but the competitive gap with Lilly has widened.

The underlying reason for Lilly’s dominance is instructive. It is not purely molecular, though tirzepatide’s dual mechanism does produce meaningfully superior weight loss. It is commercial execution. Lilly built a direct-to-consumer distribution system, committed to transparent self-pay pricing, and moved decisively to cut out the compounding market rather than cede it. Novo built a clinical evidence machine and a regulatory affairs capability without the same consumer infrastructure, and is now playing catch-up.

The lesson for the broader industry is profound. In a market where the patient pays directly, consumer brand trust, price transparency, and frictionless access matter as much as clinical efficacy. This is a pharmaceutical category that behaves like a consumer goods category. The companies and the clinical trial programs that recognize this earliest will define who wins the next decade.

The Healthy Aging Phase: The Bigger Story Hiding in Plain Sight

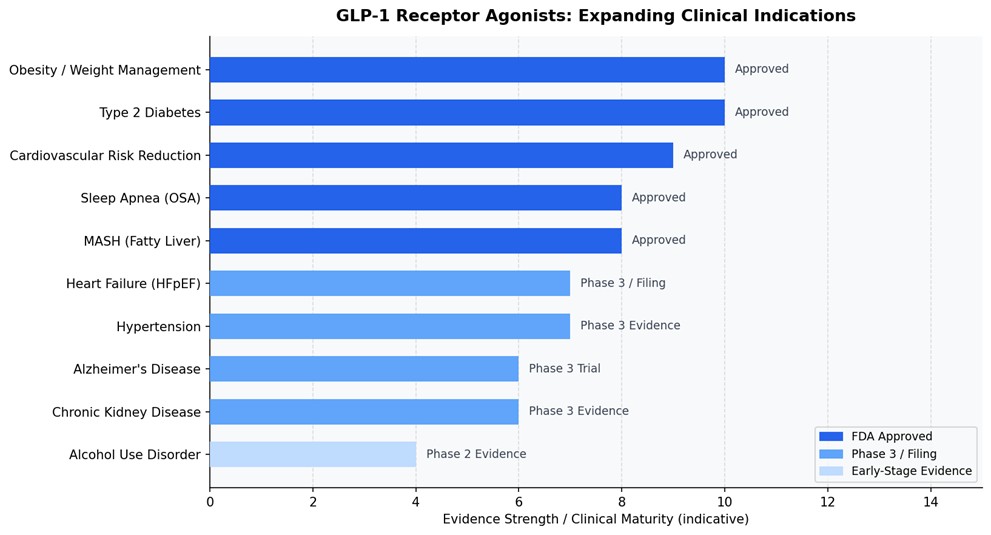

The obesity market is significant. But scientists at Novo Nordisk and Eli Lilly are increasingly making a much larger claim and the evidence behind it is accumulating faster than most investors and analysts have processed.

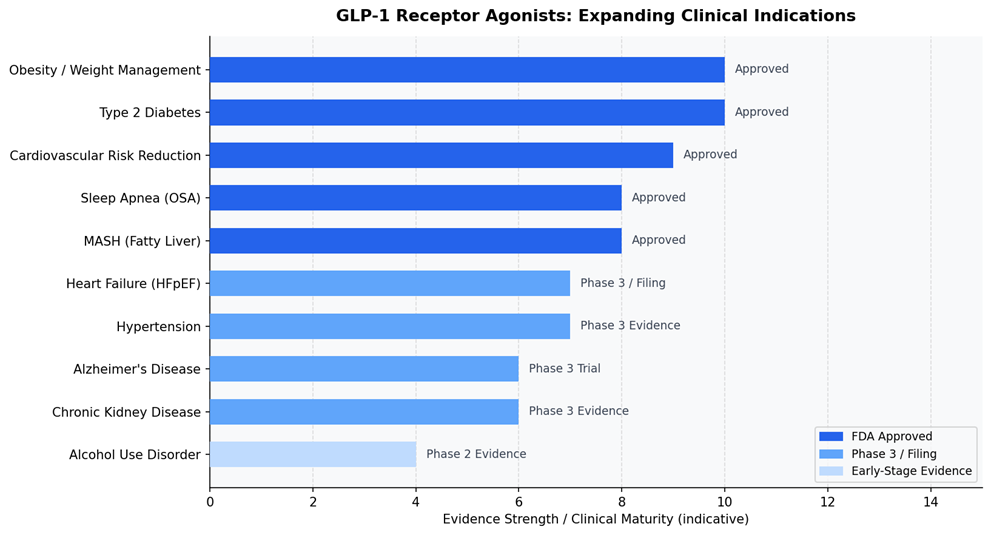

At the August 2025 Aging Research and Drug Discovery conference in Copenhagen, speakers from both companies proposed publicly that GLP-1 receptor agonists may be the first genuine longevity drugs – pharmaceuticals that target not a single disease but the biological machinery of aging itself (Nature Biotechnology, 2025). The evidence they presented spans organ systems.

Four major cardiovascular outcomes trials – HARMONY, AMPLITUDE-O, PIONEER, and SUSTAIN-6 demonstrated reductions of more than 20% in major adverse cardiovascular events in patients taking GLP-1 agonists (Cardiovascular Endocrinology & Metabolism, 2025). The SELECT trial with semaglutide showed a 20% MACE reduction specifically in obese patients without diabetes which was pivotal, because it confirmed the cardiovascular benefit does not run entirely through glucose lowering. It is something else. Semaglutide has received FDA approval for MASH – metabolic dysfunction-associated steatohepatitis with evidence showing antifibrotic effects operating independently of weight loss. GLP-1 agonists show renoprotective properties, reducing albuminuria and slowing the progression of kidney disease through natriuretic and anti-inflammatory mechanisms (Reviews in Cardiovascular Medicine, 2025). Real-world data in diabetic patients shows reduced dementia risk, and the EVOKE and EVOKE+ Phase 3 trials are evaluating semaglutide in early-stage Alzheimer’s disease in patients who do not have diabetes which suggests the neuroprotective mechanism may be entirely independent of glycaemic effects (Nature Biotechnology, 2025; Cleveland Clinic, 2025). Preclinical data shows GLP-1 receptor stimulation enhancing mitochondrial function, reducing cellular oxidative stress, and attenuating the inflammatory signalling associated with biological aging at the cellular level (ScienceDirect, 2024).

What this means for clinical development is a revolution in the breadth of imaging endpoints required.

- Liver fat quantification via MRI-PDFF.

- Hepatic fibrosis staging via MRE.

- Cardiac function via MRI.

- Renal biomarkers.

- Brain volumetrics.

- Amyloid burden via PET.

Each new indication that a GLP-1 agonist enters requires a new imaging infrastructure – standardized protocols, centralized reads, validated scoring systems, and regulatory-grade evidence.

This is not a pipeline story. It is a platform story. GLP-1 agonists are becoming the molecular scaffold of preventive medicine for adults over 45. A class of drug that addresses the root metabolic dysfunction driving cardiovascular disease, liver disease, kidney disease, neurodegeneration, and cancer risk simultaneously. The addressable population, if even a fraction of this evidence converts into approved indications, is not measured in tens of millions. It is measured in hundreds of millions.

Hypertension: The Bridge Between Disease and Wellness

Of all the non-obesity indications being built out around GLP-1s, hypertension deserves particular attention because it represents the most immediate, most commercially exploitable, and most reimbursable adjacent opportunity in the entire landscape.

Hypertension affects approximately 1.28 billion adults globally, roughly one in three people. Its overlap with obesity is not incidental; excess adiposity drives elevated blood pressure through haemodynamic pressure loading, sympathetic nervous system activation, renal sodium retention, and chronic vascular inflammation. A drug that treats both simultaneously is not a compound story. It is a systems story.

The clinical evidence is already there. GLP-1 agonists lower blood pressure through multiple mechanisms that are partly independent of weight loss – improved endothelial function, reduced arterial stiffness, direct renal natriuretic effects, and dampening of sympathetic activity. The SURMOUNT-1 trial data for tirzepatide showed a systolic blood pressure reduction of 6.2 mmHg and diastolic of 4.0 mmHg. Critically, GLP-1s begin lowering blood pressure before significant weight loss occurs, confirming an independent pharmacological mechanism (Reviews in Cardiovascular Medicine, 2025). In head-to-head comparisons of pharmacotherapies, tirzepatide produced the largest blood pressure reduction of any weight-loss agent, reducing systolic by approximately 6.5 mmHg versus placebo – comparable in magnitude to adding a mild antihypertensive.

For the pharma and biotech industry, this creates a reimbursement story that obesity alone cannot. Insurers and health systems that will not cover a weight-loss drug will often cover one that demonstrably reduces cardiovascular risk and blood pressure. The framing matters enormously. A drug positioned as treating clinical obesity with comorbid hypertension, projected to reduce MACE events and prevent hospitalizations, clears a different payer threshold than one positioned solely as a weight-loss medicine. Novo Nordisk has already filed Wegovy for heart failure with preserved ejection fraction, a condition that is substantially driven by hypertension and obesity and Ozempic has been filed for peripheral artery disease (Prime Therapeutics, 2025). The cardiovascular-metabolic corridor is being built, brick by brick.

For sponsors designing trials in this space, hypertension data is no longer a secondary endpoint footnote. It is a primary commercial asset.

When Drugs Become Wellness

There is a moment in the history of every transformative drug category when it stops being medicine and starts being culture. Statins had it in the 1990s. Oral contraceptives had it in the 1960s. GLP-1 agonists are having it now.

People are not taking Wegovy and Zepbound only because their doctor told them to. They are taking them because they want to age better, feel different, reduce risk they cannot yet measure, and live at a body weight they could not achieve through willpower alone. This is the wellness construct and it is a fundamentally different commercial and cultural framework from the traditional pharmaceutical model, where drugs treat diagnosed pathology.

Morgan Stanley analysts noted in 2025 that GLP-1 adoption is reshaping consumer behavior at a population level – how people eat, shop, exercise, and perceive themselves. A 2024 Cornell University study found that households with at least one GLP-1 user reduced grocery spending by 5.3% within six months of starting treatment (CNBC, 2025). Food companies are reformulating. Alcohol brands are tracking reduced consumption among GLP-1 cohorts. PWC has described GLP-1-driven behaviour change as one of the most significant consumer adoption trends of the decade.

Telehealth accelerated the convergence. In the KFF 2025 poll, 17% of GLP-1 users obtained their prescriptions from an online provider and medical spas and aesthetic medicine centres are already prescribing these drugs in a wellness context that would have seemed outlandish five years ago (KFF, 2025). LillyDirect is priced at $299–$449 a month, not like a hospital drug. It is priced like a premium subscription service for a health-conscious adult making an autonomous choice.

This convergence changes what clinical evidence needs to prove. When a drug is used by patients who are not sick in the conventional sense, who are using it to reduce future risk, preserve function, and optimise health – the endpoint framework must evolve. Patient-reported outcomes, body composition, metabolic biomarkers, organ fat, vascular health, and functional performance all become relevant. The regulatory agencies are watching this space carefully, and the trials that get ahead of this shift will define the evidence standards of the next generation.

The IAG Perspective: What This Means for Clinical Development

Every dimension of this transformation – the disease reclassification, the GLP-1 pipeline expansion, the indications stretching into aging, hypertension, liver disease, and neurodegeneration, converges on a single operational reality: the clinical trial programs required to support these drugs are extraordinarily complex imaging challenges.

- Assessing body composition requires DEXA, CT volumetry, and MRI.

- Measuring hepatic steatosis and fibrosis requires MRI-PDFF and MR elastography.

- Quantifying visceral versus subcutaneous fat requires standardized volumetric protocols.

- Evaluating cardiovascular endpoints requires cardiac MRI and vascular imaging.

- Staging liver disease requires not just imaging but central reads with validated scoring.

- And as GLP-1 programs move into neurodegeneration and aging, PET imaging for amyloid and tau, brain volumetrics via MRI, and longitudinal white matter tracking all enter the picture.

Designing these endpoints well from the beginning – choosing the right modalities, building the right read methodology, aligning with regulatory expectations before the protocol is locked, is what separates a successful program from an expensive detour.

At Image Analysis Group (IAG)

At Image Analysis Group that each step – from planning to execution requires scientific leadership that understands both the biology and the regulatory landscape simultaneously.

Image Analysis Group (IAG) team has been designing and delivering exactly this kind of imaging infrastructure for clinical trials since 2007, across more than 700 programs in oncology, metabolic disease, musculoskeletal, rheumatic and rare diseases. In the metabolic space specifically, where the obesity revolution is now generating intense activity – IAG and our partners bring established expertise in body composition imaging, bone health, liver fat quantification, MASH and NASH trial design, and the kind of multi-modality endpoint architecture that GLP-1 programs increasingly demand.

If you are a biotech or pharmaceutical company building a program in obesity, metabolic syndrome, MASH, cardiovascular disease, hypertension, or any of the adjacent indications where GLP-1 evidence is accumulating, the imaging strategy is not just procurement decision. It is a scientific one. Imaging is the category of critical importance, which has direct impact on trial endpoints. Getting it right at protocol stage is what creates clean, regulatorily defensible data at submission.

Reach out to our team: contact@ia-grp.com

Speak to IAG about your imaging strategy before your protocol is locked.

The decisions made at that stage — about modalities, read methodology, scoring systems, and endpoint hierarchy – will determine the quality of your data package years from now.

Contact IAG to discuss how your program can be designed for success from the ground up.

Conclusion: The Obesity Epidemic is not the Destination. It Is the Beginning.

The disease has been reclassified. The drugs are working. The market is growing at a rate that has no precedent in pharma. Two companies have been restructured entirely around this opportunity and are now among the most valuable businesses on earth. And science is pointing toward something far larger than obesity, toward a class of molecules that may address the fundamental biology of aging across multiple organ systems simultaneously.

The insurance system will catch up, eventually. Coverage will expand. Prices will continue to fall as oral formulations increase competition. The compounding market will be curtailed. And as evidence mounts for cardiovascular, neurological, hepatic, and renal benefits, the clinical and commercial case for broader reimbursement will become politically irresistible.

What is happening now – in the labs, in the trial programs, in the regulatory submissions, in the investor portfolios, and in the living rooms of patients who are paying $300 a month out of their own pockets to access a treatment they believe in, is a structural break. Not a market cycle. Not a therapeutic fashion. A permanent redefinition of what pharmacological medicine can do for the aging human body.

The companies, trial sponsors, and research organizations that position themselves correctly within this shift will not just participate in the obesity market. They will help define the evidence base of preventive medicine for the next 30 years.

Image Analysis Group is actively partnering with sponsors across the GLP-1 and metabolic pipeline —from first-in-human studies through to pivotal trials. Whether your program involves body composition, liver disease, cardiovascular endpoints, or emerging neurological indications, IAG’s imaging expertise and DYNAMIKA™ platform can support every stage of development. Reach out to IAG to explore what a purpose-built imaging strategy could do for your program.

Sources:

Goldman Sachs Insights, GrandView Research, KFF Health Policy Research, Peterson-KFF Health System Tracker, JAMA Health Forum, Eli Lilly and Novo Nordisk investor filings, BioPharma Dive, Pharmaceutical Technology, Reuters, Prime Therapeutics GLP-1 Pipeline Updates, Nature Biotechnology, Reviews in Cardiovascular Medicine, Aging Cell, IQVIA, CNBC, Walmart corporate communications, Morgan Stanley Investment Management, Cornell University, Cleveland Clinic, ScienceDirect.